The Medicare open enrollment period — a time when beneficiaries can change their coverage — began October 15 and runs through December 7. Medicare beneficiaries receive benefits either through traditional Medicare or a private Medicare Advantage (MA) plan. Deciding between these options and also among Medicare Advantage plans can be challenging: the coverage options have trade-offs, and beneficiaries have diverse needs.

Beneficiaries with traditional Medicare can see nearly any doctor and visit any hospital they choose, with no network limits or prior approval requirements. They may purchase supplemental insurance coverage, known as Medigap, to help cover cost sharing, and a Part D plan to cover prescription drugs. Beneficiaries typically have limited windows of time when they can purchase a Medigap policy without underwriting or being denied coverage.

In addition to medical coverage, Medicare Advantage plans may offer dental, vision, and hearing coverage, as well as other benefits not covered by traditional Medicare. The plans limit out-of-pocket spending on medical services and typically include Part D prescription drug coverage. Medicare Advantage plans have more limited networks of doctors and providers and usually require care to be approved beforehand, a practice known as prior authorization.

Choosing coverage is further complicated by the number of insurers and available plans. In 2025, the average beneficiary is expected to be able to choose among 34 Medicare Advantage and 15 stand-alone Part D plans. Beneficiaries also receive marketing and outreach from plans, brokers and agents, and third-party marketing organizations.

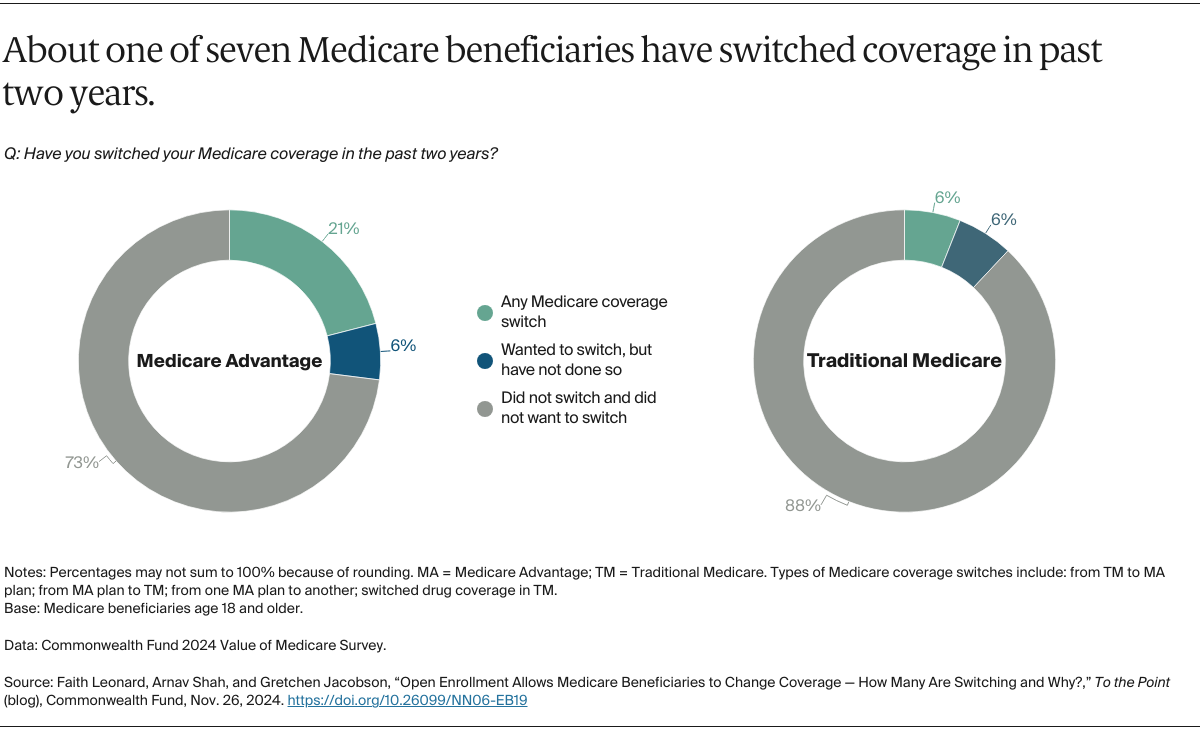

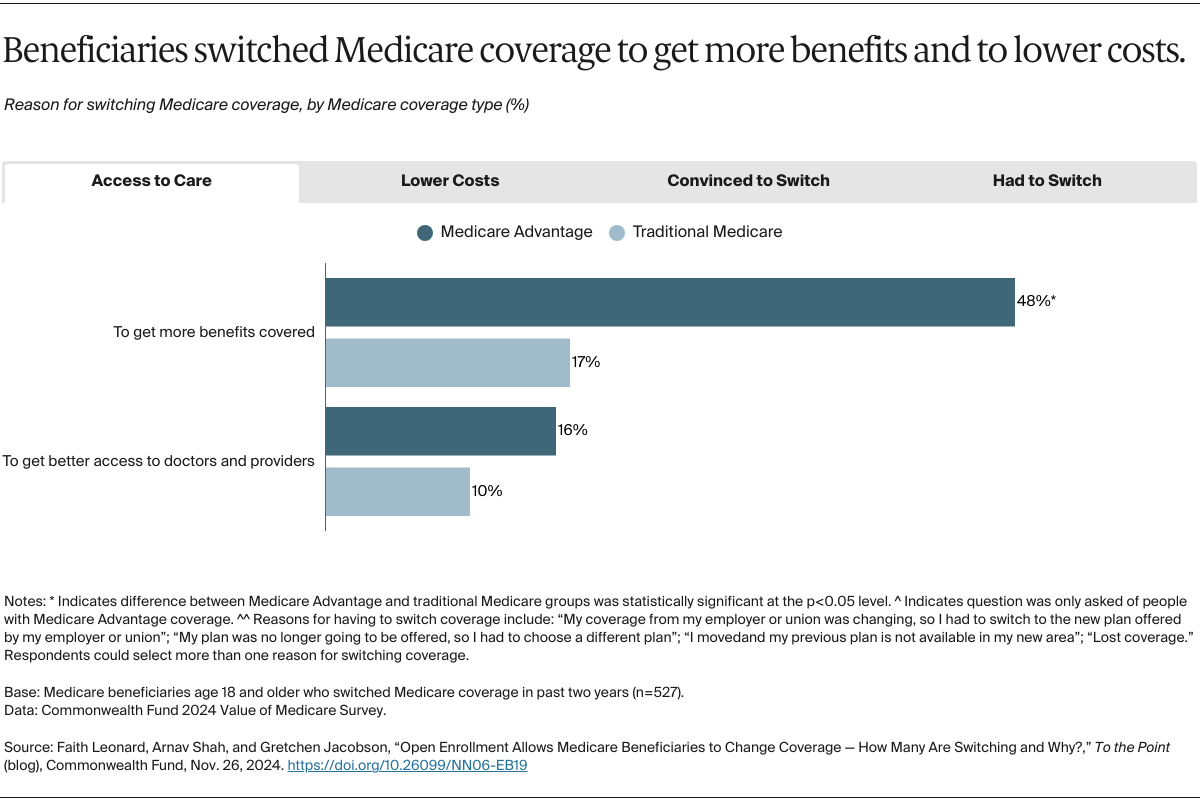

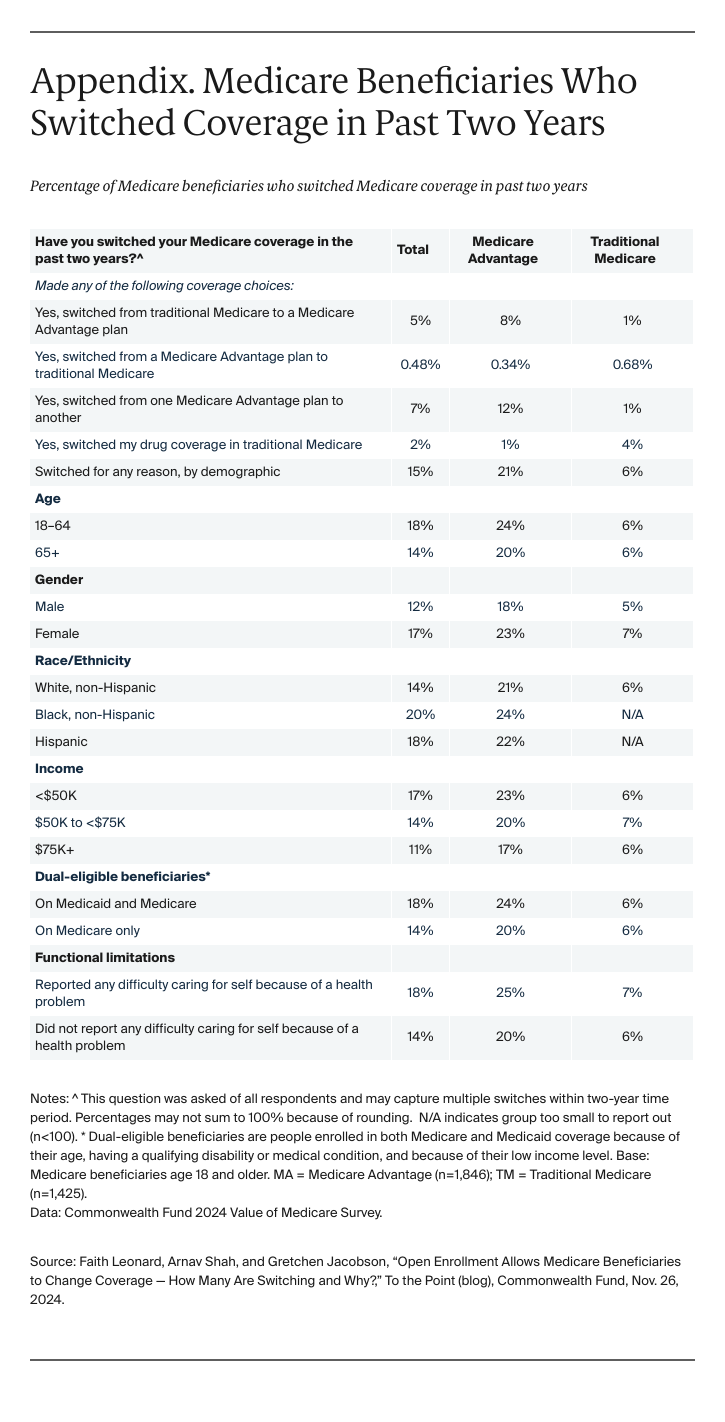

To find out who is switching Medicare coverage, what types of changes they are making, and the reasons behind those decisions, we looked at data from the Commonwealth Fund 2024 Value of Medicare Survey (for more detail, see “How We Conducted This Survey”).